Variable-rate mortgages in Canada are now averaging about 4.20%, a full percentage point higher than they were a week ago.

That’s thanks to the Bank of Canada’s latest 100-bps rate hike, which was followed by an equal increase in the prime rate, upon which variable mortgages and lines of credit are priced.

Steve Huebl

What next?

The prime rate at most lenders is now 4.70%, a level not seen since 2008, and up from 2.45% at the start of the year.

“I think the big takeaway here is what it’s going to do to the variable-rate mortgage segment,” Steve Saretsky, a Realtor at Oakwyn Realty, told BNN Bloomberg in an interview. “At the end of the day, we’ve seen a huge cohort of people—more than 60% of purchasers over the last year and a half—going [into] variable-rate mortgages.”

Saretsky added that on top of the 100-basis-point rate hike, new variable-rate borrowers will have to qualify at a stress test rate of 200 bps above their contract rate as opposed to the minimum of 5.25% (something fixed-rate borrowers have had to do ever since fixed rates rose above the 3.25% threshold). Stress test rules for both insured and uninsured mortgages mean borrowers must prove they can afford payments based on their contract rate plus 2% or 5.25%, whichever is higher.

“Now they’re getting stress-tested effectively at about 6.20%, 6.25%,” Saretsky said. “That again will reduce purchasing power and that will feed through to the housing market.”

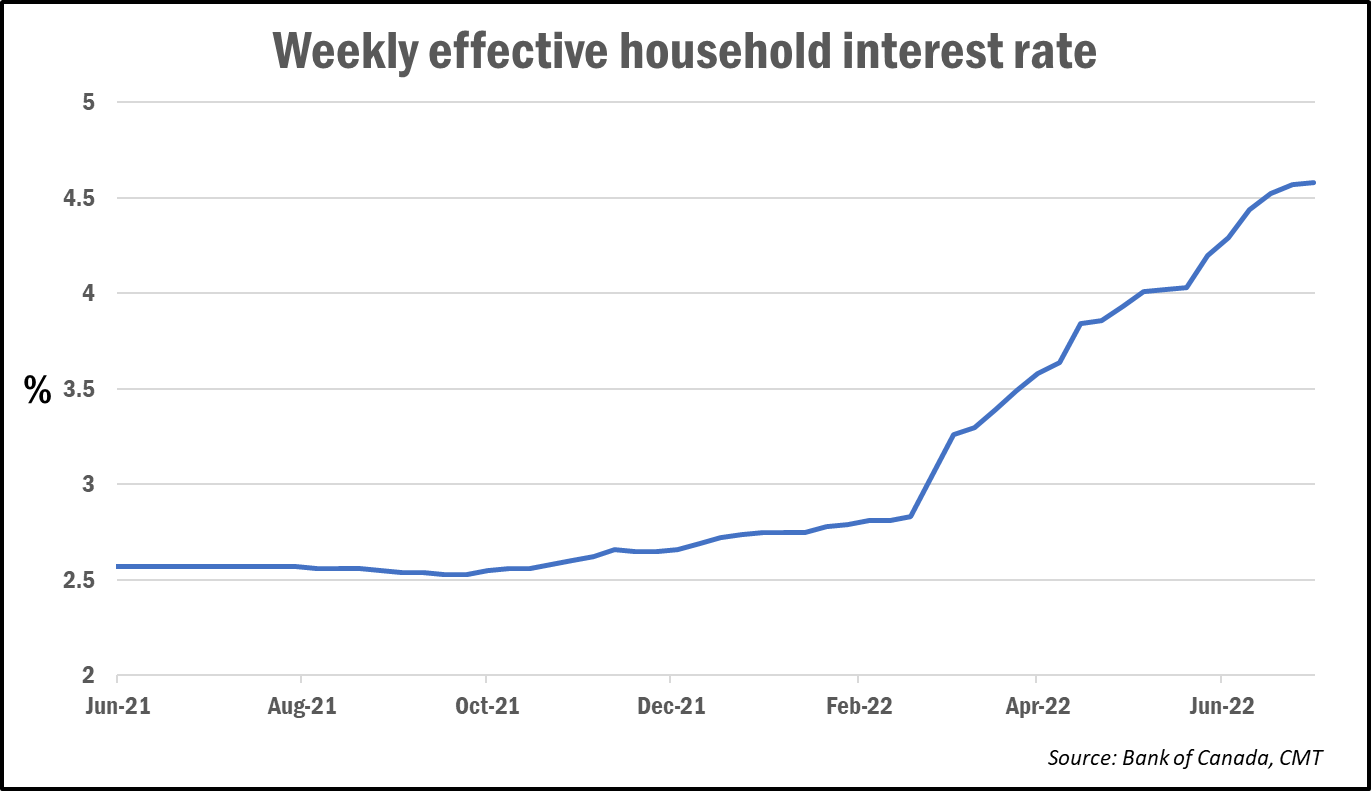

Looking at the bigger picture, overall carrying costs for Canadian consumers have surged since the start of the year.